Using a centralized IFRS9 model architecture and Python to reduce BAU operating expenses by up to 40%

15 February 2022

Our previous Insights article explained how banks could reduce IFRS9 model development and implementation costs by about 30% using a centralised credit model architecture for wholesale portfolios. Centralised model architectures improve substantially on the two-stage IRB-IFRS9 approach common to banks today. In this follow-up article we highlight the IFRS9 BAU operating expense reductions available from utilising an E2E open-source Python approach to IFRS9 implementation.

Read and download the full article >>

we highlight the IFRS9 BAU operating expense reductions available from utilising an E2E open-source Python approach to IFRS9 implementation. Reduced IFRS9 operating expenses, combined with reduced development and implementation expenses therefore in the aggregate, can save banks a substantial amount of money. A centralized IFRS9 solution also provides a more accurate and dynamic credit model ecosystem to support an uncertain risk environment, that today is complicated by a combination of covid, climate and regulatory compliance.

To estimate potential operating expense savings, like the first Insights article we undertake an illustrative benchmark exercise for a large, hypothetical European Bank. Like all banks in Europe, the EBA Repair Initiative currently requires all IRB models to be redeveloped. This effort therefore provides an interesting opportunity to re-think both IFRS9 methodology and implementation, providing enhanced risk management benefits to go with the substantial IFRS9 expense reductions. There is a clear evolution in bank’s implementation of complex credit models, which is moving away from more expensive, external vendor solutions and toward open-source internally managed platforms like Python.

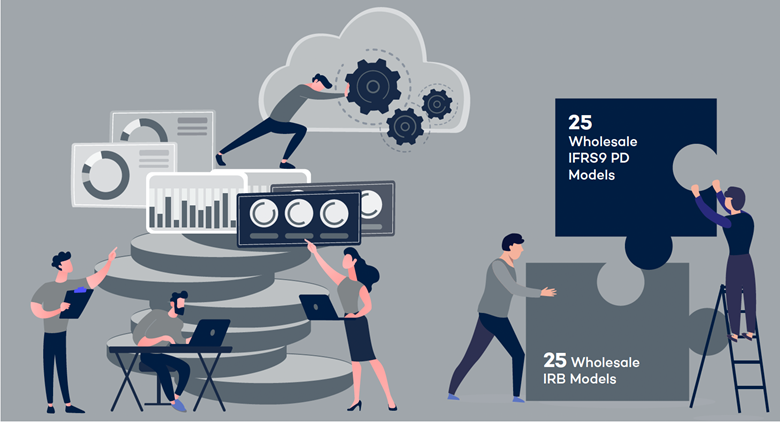

The Figure below provides a graphic to illustrate the general implementation approach common to bank’s using two-stage IFRS9 model:

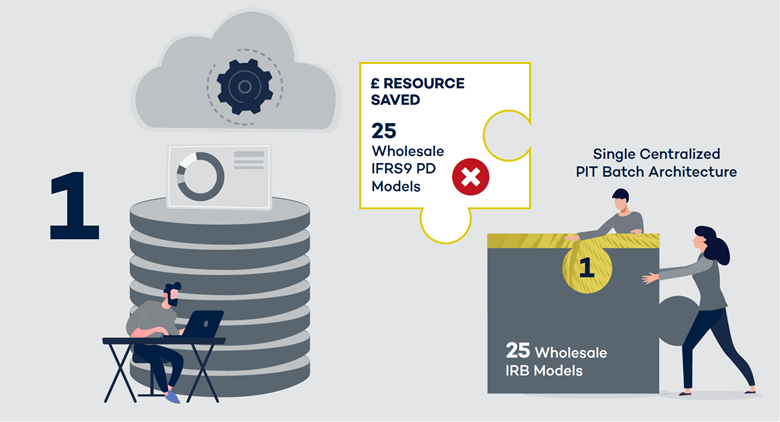

As an alternative we outline a centralised implementation approach for IFRS9 that uses a single, holistic PIT/TTC methodology that applies credit cycle adjustments to all of a bank’s IRB model outputs in a single batch process:

Read and download the full article >>